Your CIBIL score plays a crucial role in your financial life. Whether you're applying for a personal loan, home loan, credit card, or even negotiating better interest rates, lenders closely examine your credit score before making decisions.

The good news is that improving your CIBIL score doesn't always take years. By following the right strategies consistently, you can significantly improve your credit profile and increase your chances of loan approvals much faster than most people think.

In this comprehensive guide, you'll discover 15 proven tips that can help improve your CIBIL score quickly while building long-term financial credibility.

Understanding CIBIL Score and Why It Matters

1. What Is a CIBIL Score?

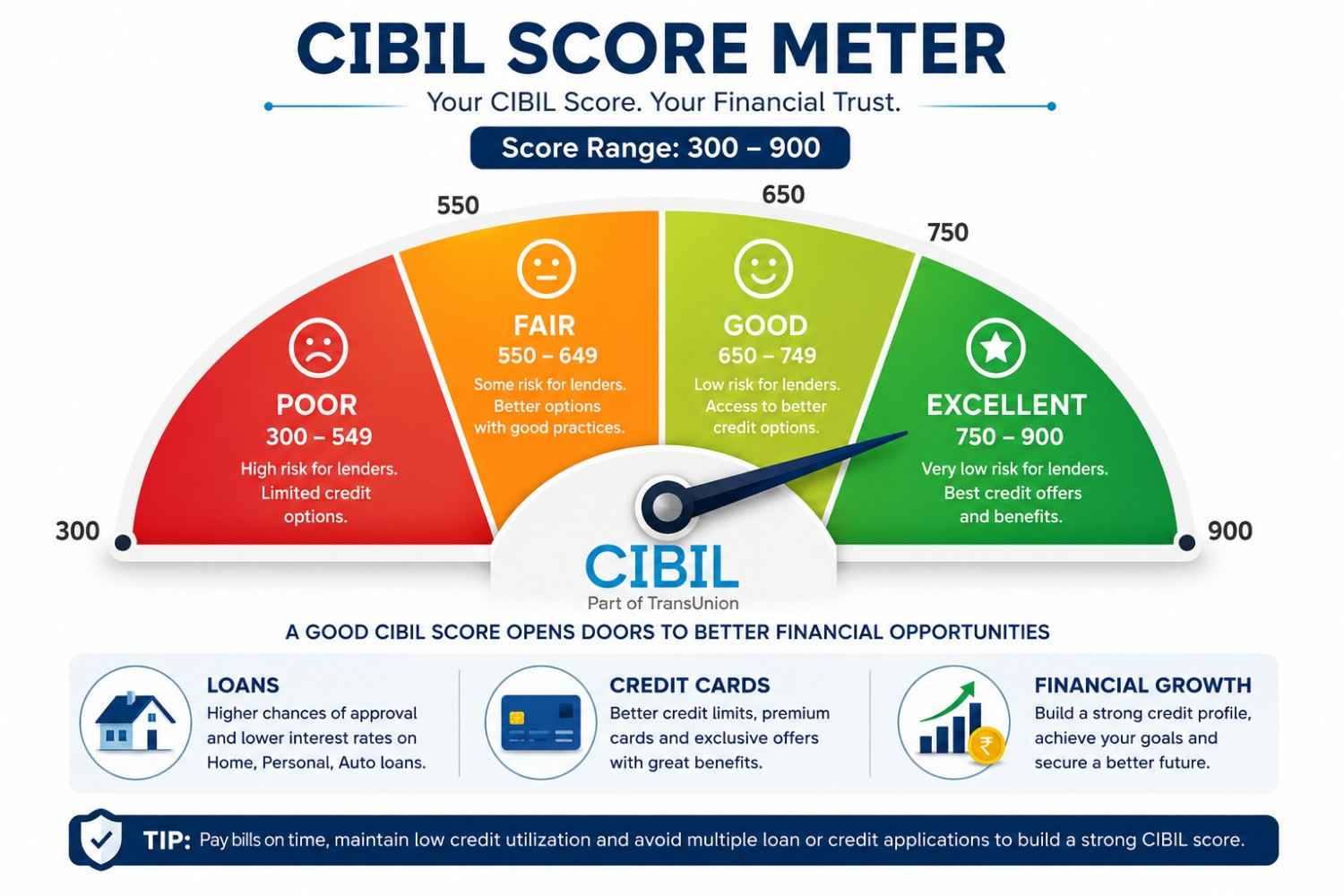

A CIBIL score is a three-digit number ranging from 300 to 900 that reflects your creditworthiness. It is calculated based on your credit history, repayment behavior, credit utilization, and borrowing patterns.

Generally:

- 750 and above: Excellent

- 700–749: Good

- 650–699: Fair

- Below 650: Needs improvement

2. Why Banks Check Your CIBIL Score

Financial institutions use your CIBIL score to assess risk before approving:

- Personal loans

- Home loans

- Car loans

- Credit cards

- Business loans

A higher score often means:

- Faster loan approvals

- Lower interest rates

- Higher credit limits

- Better financial opportunities

Check Your Credit Report for Errors

1. Download Your Latest Credit Report

The first step toward improving your CIBIL score is understanding your current situation. Obtain your latest credit report and carefully review every detail.

Look for:

- Incorrect loan amounts

- Duplicate accounts

- Wrong personal information

- Closed loans marked as active

- Unauthorized credit inquiries

2. Dispute Any Incorrect Information Immediately

Even small errors can negatively impact your credit score.

If you find inaccuracies:

- File a dispute with the credit bureau.

- Submit supporting documents.

- Follow up regularly until the issue is resolved.

Correcting reporting errors can sometimes increase your score surprisingly quickly.

Pay All EMIs and Credit Card Bills on Time

1. Payment History Has the Highest Impact

Your payment history contributes significantly to your CIBIL score calculation.

Missing even one payment can:

- Reduce your credit score

- Remain on your report for years

- Affect future loan approvals

Always prioritize timely payments.

2. Set Up Automatic Payments

To avoid accidental delays:

- Enable auto-debit facilities

- Set calendar reminders

- Maintain sufficient account balance

- Use banking alerts

Consistency in payments gradually rebuilds trust with lenders.

Reduce Your Credit Utilization Ratio

1. Understand Credit Utilization

Credit utilization refers to the percentage of available credit you use.

Example:

- Credit limit: ₹100,000

- Usage: ₹80,000

- Utilization ratio: 80%

Experts recommend keeping utilization below 30%.

2. Strategies to Lower Utilization Quickly

You can reduce utilization by:

- Paying outstanding balances early

- Making multiple payments monthly

- Requesting higher credit limits

- Avoiding unnecessary spending

Lower utilization often leads to faster improvements in your credit score.

Avoid Applying for Multiple Loans Simultaneously

1. Every Loan Application Creates a Hard Inquiry

When you apply for credit, lenders perform a hard inquiry.

Too many inquiries indicate:

- Financial stress

- Increased borrowing risk

- Poor credit management

This can reduce your score.

2. Space Out Your Applications

Instead of applying everywhere:

- Research eligibility first

- Apply only when necessary

- Wait several months between applications

Selective borrowing improves your credit profile.

Clear Outstanding Debts Strategically

1. Focus on High-Interest Debt First

If you have multiple debts, prioritize:

- Credit card debt

- Personal loans

- High-interest borrowings

Reducing expensive debt helps both your finances and credit score.

2. Consider Debt Consolidation

Debt consolidation combines multiple debts into one manageable payment.

Benefits include:

- Simplified repayment

- Lower interest burden

- Reduced missed payments

- Better financial discipline

Keep Old Credit Accounts Active

1. Credit History Length Matters

Older accounts demonstrate long-term financial responsibility.

Closing old accounts may:

- Reduce your average account age

- Lower available credit

- Negatively impact your score

2. Use Older Cards Occasionally

Maintain older credit cards by:

- Making small purchases

- Paying bills on time

- Keeping balances low

This preserves your credit history.

Maintain a Healthy Credit Mix

1. Understand Credit Diversity

Lenders prefer borrowers who manage different types of credit responsibly.

Examples include:

- Home loans

- Personal loans

- Auto loans

- Credit cards

- Consumer durable loans

2. Avoid Overdependence on One Credit Type

Relying solely on credit cards can increase risk perception.

A balanced credit portfolio signals responsible financial behavior.

Increase Your Credit Limit

1. Higher Limits Reduce Utilization

Requesting a credit limit increase can improve your utilization ratio immediately.

Example:

| Credit Limit | Outstanding Balance | Utilization |

|---|---|---|

| ₹100,000 | ₹50,000 | 50% |

| ₹200,000 | ₹50,000 | 25% |

Lower utilization often supports higher scores.

2. Request Increases Carefully

Before requesting:

- Maintain good repayment history

- Avoid recent defaults

- Ensure stable income

Banks are more likely to approve responsible customers.

Avoid Settling Loans If Possible

1. Settlement Impacts Credit Score

When you settle a loan for less than the full amount, lenders record it as "settled" rather than "closed."

This may:

- Reduce lender confidence

- Lower creditworthiness

- Affect future borrowing opportunities

2. Aim for Full Closure

Whenever possible:

- Pay the entire outstanding amount

- Obtain a No Objection Certificate (NOC)

- Ensure records reflect "closed"

Monitor Your Credit Report Regularly

1. Monthly Monitoring Helps

Frequent monitoring allows you to:

- Detect fraud early

- Track progress

- Correct errors quickly

- Improve financial awareness

2. Create a Credit Improvement Plan

Track:

- Payment dates

- Debt reduction goals

- Credit utilization levels

- Score improvements

Regular monitoring accelerates progress.

Become an Authorized User

1. Benefit from Strong Credit Profiles

If a trusted family member has excellent credit history, becoming an authorized user on their account may positively influence your profile.

2. Choose Carefully

Ensure the primary account holder:

- Pays bills on time

- Maintains low balances

- Has a long credit history

Poor account behavior can also negatively affect you.

Avoid Frequently Closing Credit Cards

1. Closing Cards Can Reduce Scores

Closing cards may:

- Increase utilization ratios

- Shorten credit history

- Reduce available credit

2. Keep No-Fee Cards Open

If a card has no annual fee, consider keeping it active with minimal usage.

Use Secured Credit Cards to Rebuild Credit

1. Secured Cards Help Establish Credit

If your score is very low, secured credit cards can help rebuild credit history.

These cards require a fixed deposit as security.

2. Practice Responsible Usage

To maximize benefits:

- Spend minimally

- Pay balances fully

- Avoid late payments

Over time, this improves your credit profile.

Resolve Loan Defaults Immediately

1. Outstanding Defaults Severely Damage Scores

Defaults are among the most damaging factors affecting credit scores.

They indicate:

- Financial instability

- Increased lending risk

2. Negotiate Repayment Plans

If repayment is difficult:

- Contact lenders early

- Request restructuring

- Create realistic repayment schedules

Resolving defaults significantly improves long-term credit health.

Maintain Financial Discipline Consistently

1. Build Healthy Financial Habits

Successful credit management requires:

- Budgeting

- Controlled spending

- Emergency savings

- Responsible borrowing

2. Think Long-Term

Improving your CIBIL score isn't only about getting loans. It's about building lifelong financial credibility and freedom.

Consistent habits produce sustainable results.

How Fast Can You Improve Your CIBIL Score?

1. Typical Improvement Timeline

Improvement speed depends on your financial situation:

| Action | Estimated Impact Timeline |

| Correcting report errors | 30–60 days |

| Reducing utilization | 30–90 days |

| Paying overdue accounts | 3–6 months |

| Building payment history | 6–12 months |

| Recovering from defaults | 12–24 months |

2. Patience and Consistency Matter

Quick improvements are possible, but maintaining healthy credit habits is the key to long-term success.

FAQ

1. What is the fastest way to improve a CIBIL score?

The fastest methods include paying overdue balances, reducing credit utilization below 30%, correcting credit report errors, and avoiding new loan applications.

2. Can my CIBIL score improve in 30 days?

Yes. If you reduce outstanding credit card balances or successfully correct reporting errors, you may notice improvements within 30 to 60 days.

3. Does checking my own CIBIL score reduce it?

No. Checking your own credit report is considered a soft inquiry and does not affect your credit score.

4. Is 750 a good CIBIL score?

Yes. A score of 750 or above is generally considered excellent and increases your chances of obtaining loans and credit cards on favorable terms.

5. How long do late payments affect a CIBIL score?

Late payments can remain on your credit report for several years, although their impact decreases over time if you maintain consistent repayment behavior afterward.

Conclusion

Improving your CIBIL score quickly is possible when you focus on the factors that matter most: timely payments, low credit utilization, responsible borrowing, and regular credit monitoring. While some improvements can happen within weeks, lasting financial credibility requires consistency and discipline.

Start implementing these 15 proven strategies today. Every positive financial decision you make strengthens your credit profile and brings you closer to better loan approvals, lower interest rates, and greater financial freedom.

Write a comment