Choosing the right savings account in 2026 is no longer just about convenience. With interest rates varying significantly across banks, the difference between earning 2.5% and 6.5% annually can substantially impact your returns over time. While traditional banks continue offering lower but stable rates, several private and small finance banks are competing aggressively for deposits by offering much higher yields.

If you're planning to park your emergency fund, salary savings, or short-term investments, understanding the latest savings account interest rates can help maximize returns without compromising liquidity. This guide covers the best savings account interest rates in India as of August 2026, compares major banks, and explains how to choose the right account for your financial needs.

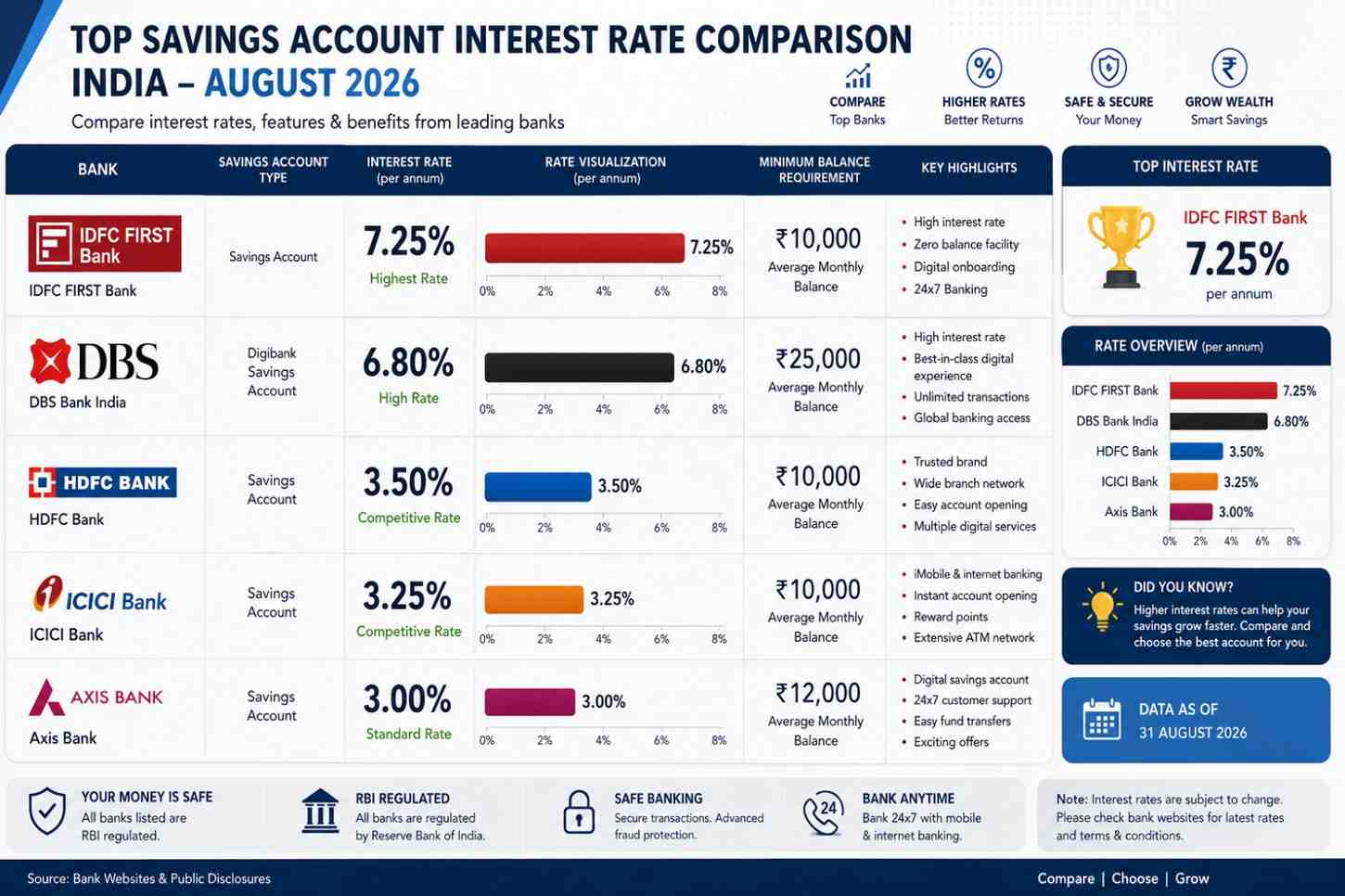

Best Savings Account Interest Rates in India (August 2026)

1. Top Savings Account Interest Rate Comparison

| Bank | Interest Rate (p.a.) | Applicable Balance |

|---|---|---|

| IDFC FIRST Bank | Up to 6.50% | Above ₹3 lakh up to ₹25 crore |

| DBS Bank India | Up to 5.00% | ₹2 lakh to ₹50 lakh |

| Standard Chartered Bank | Up to 5.00% | Large balance slabs |

| Axis Bank | Up to 3.50% | Select balance slabs |

| ICICI Bank | 2.50% | All balances |

| HDFC Bank | Up to 3.50% | Select balance slabs |

| Bank of India | 2.50%–3.30% | Based on balance slabs |

Rates are subject to revision by banks and may vary depending on account type and balance maintained.

Why Savings Account Interest Rates Matter in 2026

1. Inflation Reduces Idle Cash Value

Money sitting in a low-interest savings account gradually loses purchasing power due to inflation. Earning higher interest helps offset this effect.

2. Emergency Funds Should Still Earn Returns

Most financial planners recommend keeping six to twelve months of expenses in liquid assets. A high-interest savings account allows your emergency fund to remain accessible while generating returns.

3. Higher Rates Compound Over Time

Even a 2–3% difference in annual interest rates can translate into significant gains over several years, especially for larger balances.

Best Banks for High Savings Account Interest

1. IDFC FIRST Bank

IDFC FIRST continues to offer one of the highest savings account rates among major private banks in India. Its progressive interest rate structure benefits customers maintaining balances above ₹3 lakh. The bank also provides unlimited ATM withdrawals and strong digital banking features.

2. DBS Bank India

DBS Bank offers attractive rates for balances between ₹2 lakh and ₹50 lakh, combined with a fully digital banking experience. It remains a popular choice among urban professionals seeking convenience and competitive returns.

3. Small Finance Banks

Several small finance banks continue to offer savings account rates above 5%, and in some cases close to 6%. However, customers should understand balance slabs, liquidity needs, and deposit insurance limits before concentrating large amounts with a single institution.

Traditional Banks vs High-Interest Banks

1. Traditional Banks

Traditional banks such as SBI, HDFC Bank, ICICI Bank, and Axis Bank offer:

- Greater branch presence

- Established customer service networks

- Higher perceived safety

- Better integration with salary accounts

The trade-off is relatively lower interest rates.

2. High-Interest Banks

High-interest savings accounts generally provide:

- Better returns

- Digital-first experience

- Competitive features

- Attractive onboarding offers

However, they may have:

- Balance slabs

- Limited physical branches

- Variable interest policies

How to Choose the Best Savings Account

1. Consider Your Average Balance

If your savings remain below ₹50,000, a bank offering high rates only above ₹3 lakh may not benefit you.

2. Evaluate Digital Banking Features

Look for:

- Mobile app quality

- UPI support

- Instant transfers

- Online account opening

- Customer support responsiveness

3. Check Additional Charges

Review:

- Minimum balance requirements

- ATM withdrawal fees

- Debit card charges

- Non-maintenance penalties

4. Understand Deposit Insurance

Bank deposits in India are insured up to ₹5 lakh per depositor per bank under the DICGC framework. Diversification across banks can reduce concentration risk.

Should You Keep Large Amounts in Savings Accounts?

1. For Emergency Funds

Yes. Emergency funds require liquidity and safety.

2. For Long-Term Wealth Creation

No. For long-term goals, consider alternatives such as:

- Fixed deposits

- Debt mutual funds

- Equity mutual funds

- Government securities

- Hybrid investments

Savings accounts prioritize liquidity over maximum returns.

Savings Account vs Fixed Deposit

| Feature | Savings Account | Fixed Deposit |

|---|---|---|

| Liquidity | Very High | Limited |

| Interest Rate | 2.5%–6.5% | 6%–8%+ |

| Lock-in | None | Fixed tenure |

| Risk | Very Low | Very Low |

| Best For | Emergency funds | Long-term savings |

Fixed deposits continue offering higher yields than savings accounts in 2026, particularly through small finance banks.

Common Mistakes to Avoid

1. Choosing Only Based on Interest Rate

The highest advertised rate may apply only to a specific balance range.

2. Ignoring Hidden Charges

Account maintenance charges can offset interest gains.

3. Keeping Excess Cash Idle

Large idle balances earning low returns can reduce long-term wealth accumulation.

4. Concentrating All Savings in One Bank

Diversification improves financial safety and flexibility.

FAQ

1. Which bank offers the highest savings account interest rate in India in August 2026?

Among major private banks, IDFC FIRST Bank offers one of the highest savings account interest rates, reaching up to 6.5% per annum on eligible balance slabs. Some small finance banks may offer even higher rates depending on account conditions.

2. Are savings account interest rates fixed?

No. Savings account interest rates are variable and can change based on RBI policy decisions and bank-specific strategies.

3. Is money in savings accounts safe?

Yes. Scheduled banks regulated by the Reserve Bank of India are generally considered safe, and deposits up to ₹5 lakh per depositor per bank are insured under DICGC.

4. Should I choose a small finance bank for higher interest?

Small finance banks can offer excellent returns, but diversification and understanding deposit insurance limits remain important considerations.

5. Is a savings account better than a fixed deposit?

Savings accounts are better for liquidity and emergency funds, while fixed deposits typically provide higher returns for long-term savings goals.

Conclusion

The best savings account in India during August 2026 depends on your priorities. If maximizing returns is your primary objective, banks like IDFC FIRST Bank and select small finance banks remain strong choices. If convenience, branch access, and stability matter more, established institutions such as HDFC Bank, ICICI Bank, and Axis Bank continue to be reliable options.

A practical strategy for many savers is to maintain a primary account with a large established bank while parking surplus funds in a higher-interest savings account within deposit insurance limits. This approach balances safety, convenience, and returns effectively.

Write a comment